When it comes to banking, today we have much more choice as to who looks after our money. But the biggest players are also providing us with incredible money management tools. Michael Barton puts this market leader to the test in his Monzo review, to help you decide if it’s the bank for you.

Post date

Post author name

Michael Barton

This article has been fact checked by a member of the Wallet Savvy editorial team and complies with our editorial standards.

Wallet Savvy is a reader supported website. This means that some pages include links to products or services that we recommend and we may earn a commission when you make a purchase. You will never pay more by choosing to click through our links.

Spoiler alert! I don’t have a Monzo account, but my son and daughter-in-law do. They love it. Are they right in their conclusion? I decided to take a look and see if what they were telling me was true. I wanted to know if I should become a Monzo customer myself.

In this Monzo review, you will learn all you need to decide if a Monzo account would be best for you.

(Editor’s Note: All types of accounts, their fees and their rates, have been checked and updated on 31/05/2024.)

Quick Verdict On Monzo

Monzo’s branchless, app-driven approach provides you with a modern, user-friendly experience. It can revolutionise your relationship with budgeting, spending, and saving. There’s a whole gamut of banking features for you to benefit from, and certainly more than most (if not all) traditional high street banks.

It’s easy to open an account, and you’ll find the app delivers a refreshingly clean experience. While there is a free account which is ideal for first-timers new to online banking, the paid-for accounts each offer a good step up in features and benefits.

We’ve got a feeling that once you log on to Monzo and use your account for the first time, you won’t look back.

Monzo – A Bank Without Branches

Monzo started life in 2016. Back then it was no more than a prepaid Mastercard. You could top up your balance via the Monzo app, and use the card to make free cash withdrawals. About as exciting as watching a kettle boil. Nothing different to what you could get from any bank card, really.

Even back then, though, it had the credentials that promised more. Its founders were Jason Bates, Tom Blomfield, Gary Dolman, Jonas Huckestein, and Paul Rippon – all ex-employees of Starling Bank. It wasn’t long before it had given birth to something of a cult following, and received authorisation from the FCA, together with a banking license, in 2017.

Today, Monzo is one of a group of challenger banks – smaller banks that are disrupting the traditional banking system and doing things differently. You can’t get much more different than being a bank with no branches. Its entire infrastructure is online, and to be a customer you’ll need a smartphone to manage your money.

When I first became aware of the growth in this type of bank, I have to admit I was sceptical. But, thinking about it, what is there to be sceptical about?

The majority of people in the UK have smartphones – you may even be reading this review on yours now. Most of us are now comfortable with mobile apps. You might play games on your phone, book hotel rooms and flights while on the go, have social media accounts, and keep in touch with your friends and family through WhatsApp.

Many of us also use the online banking apps provided by the high street banks. I very rarely use a bank branch now. I think I had to go into one about three years ago to get a new PINsentry device. Then it had to be posted to my home address.

Then a few months ago, I walked into a branch of my bank because I needed to withdraw more money than the ATM would allow. They didn’t have cash behind the cash counter. But the teller solved the problem for me. He walked me through how to change my cash withdrawal limit… on my banking app!

No branches? No bother!

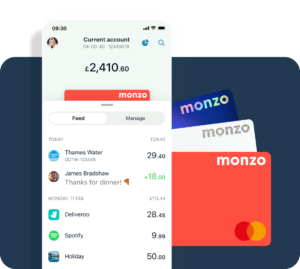

Monzo Features

Perhaps the most appealing thing about Monzo is just how much you can do on it, and how easy it makes managing your finances. This was incredibly important to my son who, up until the last few years, had not been great at managing his cash flow.

So, what can you do with a Monzo account? Here’s a list of the main features:

Budgeting, Saving, & Spending

Salary Sorter

When I pay myself, the first thing I do is sort my salary out into different ‘jars’ or ‘pots’. This separates my savings, necessary spending (utility bills, insurances, and so on), and what I have left over. It’s a manual process that requires me to make around a dozen transfers in total.

Monzo’s Salary Sorter lets you set up your pots and preferences. You then can sort your salary into them. Once you have done this, you can set it up to make these transactions automatically when your salary gets paid into your Monzo current account.

Savings Pots

We all have unique savings goals, and usually several. With Monzo, you can set up several savings pots and transfer money into them either regularly or when you have the money available. (The best way is to budget to save by paying yourself first.)

Set up different pots for each savings goal you have – Christmas savings, saving for car insurance, holidays… whatever you wish to save for.

Bills Pots

Similar to savings pots – set up your bills pots, and transfer money into them when your salary is paid into your account. Direct debits and standing orders will be separated, and you’ll never not have the money to pay them. The best part is that it can all be automated.

Monzo Flex

Here’s something a little different: Monzo Flex. This is a buy now pay later facility. Buy what you want today, and pay in instalments over 3, 6, or 12 months. Great for taking advantage of sales and managing your cashflow, but make sure you follow the buy now pay later rules.

Budgeting Controls

Creating an effective budget is a key step to achieving your financial goals. Managing that budget effectively is crucial. Monzo has tools to help you set, manage, and monitor your budget, tracking how well you are doing on your monthly spending limits.

Roundups

When we used to pay for everything in cash, I would put all my loose change in a pot each night. It was amazing how quick that could accumulate to a tidy sum. Now most spending is on card, we don’t do this. Instead, we spend every last penny.

Roundups are Monzo’s way of helping you to save your change. It’s a simple idea. Each time you spend on your card, the bill is rounded to the next pound. The difference between this and the amount you actually spent is automatically transferred into a savings pot. Simple, effective, and automatic. You won’t miss the pennies, but you will be thankful for the pounds.

Split Bills

Have you ever been to a restaurant with friends or family, and then had that embarrassing end-of-meal ‘how are we going to pay?’ conversation. It’s not that none of you have the money, it’s that you all want to pay separately. The waiter is not a happy bunny.

With Monzo, all you need to do is pay on your Monzo card and split the bill through its ‘Shared Tabs’ facility. Great for settling a bill easily and tracking who owes what.

Get Paid Early

Back in the day when bank managers knew you by first name, it was possible to phone your bank manager and arrange a temporary overdraft for a few days before your salary hit your account. I did it several times. Now, “the computer says no”.

Enter Monzo’s ‘Get Paid Early’. You can have your salary credited to your account a day early. Perfect if you accidentally go overdrawn just before payday.

Mortgages, Loans, & Overdrafts

As a bank, Monzo can offer credit to its customers. How much you can borrow depends upon your personal circumstances, but Monzo can arrange overdrafts and provide personal loans of up to £25,000.

However, interest rates are high (for example, overdraft rates range from 19% to 39% EAR). If you need to borrow money, there are cheaper options available.

If you have a mortgage, you can connect your mortgage to Monzo and track how much you owe. This could help you to identify potential to overpay (saving you interest) as well as seeing your progress on debt repayment.

Using Monzo Abroad

Monzo is also a great choice if you travel abroad. My son and daughter-in-law only use this now when they take holidays in Europe. Here’s why:

Great Foreign Exchange Rates

Monzo has partnered with Wise (of whom I am a big fan). You can send money internationally with no hidden fees. Wise also uses the Interbank rate to exchange between currencies – meaning you change your sterling for euros at the same rate at which the banks trade between each other.

No Transaction Fees

You can use your Monzo card just as you would in the UK, and pay no transaction fees or exchange fee markups as you might with other cards.

Free Cash Withdrawals While Abroad

It’s not always possible to pay by card when you’re abroad. Monzo allows you to withdraw cash free of charge from ATMs in the EEA and £200 per month elsewhere.

Saving with Monzo

Let’s look a little closer at how Monzo helps you to save. There are four types of savings pots that you can use in Monzo:

Instant Access

Earn up to 4.60% interest and retain immediate access to your cash. There is no minimum deposit requirement with Monzo’s Instant Access accounts.

Easy Access

These accounts allow you to withdraw money with one business day’s notice. The minimum deposit is £10, and you’ll earn up to 4.55% interest in an account provided by Paragon.

Easy Access Cash ISA

Earn interest tax-free, with interest rates of up to 4.77%. Like the Easy Access accounts, you can withdraw the following day. You can deposit from as little as £10 at any time. Monzo uses four providers to offer these accounts.

Fixed-Rate Savings

You can earn almost 5% in interest on Monzo’s range of Fixed-Rate Savings accounts, though you will be locking your money up for between 6 and 12 months. During this period, you cannot deposit or withdraw any money. A lump sum of at least £500 is required to open one of these accounts, which are offered via various third-party providers.

Monzo Loans

If you need to borrow money, Monzo offers a fast online application process with loans of up to £25,000 available. To assess your borrowing entitlement, Monzo asks three questions without affecting your credit rating. They promise that if accepted, your loan application:

- Will take only 5 minutes

- Will credit your account on the same day as the application is made

- Will incur no fees for early repayment

Interest payable depends upon your application and financial status, though tends to range between around 14% APR and 26% APR.

Monzo Overdrafts

If you overspend in your Monzo account and go into the red, you’ll be charged no more than £15.50. Monzo says it will notify you before you fall into an overdraft, giving you until midnight to deposit funds and avoid an overdraft situation.

If you think you are likely to go overdrawn, it is always best to arrange an overdraft. Like applying for a Monzo loan, it’s an easy online process. The maximum overdraft is £2,000, but how much you can go overdrawn by depends on your credit score. Interest charged will range from 19% to 39%.

| Tip If you need extra cash, consider applying for a Monzo loan instead of an overdraft. The interest rate is lower, and with no penalties to repay early, it could be a cheaper option for you – though you should always check the numbers before deciding. |

Monzo Flex

Buy now pay later deals (BNPL) can help you to manage your cashflow more effectively. They also give you the ability to buy something that is on sale today but will rise in price soon, even if you don’t have the cash now.

Here is how Monzo’s Flex works:

- Apply online for Monzo Flex. Monzo will run a soft credit check to assess eligibility. This won’t affect your credit score.

- If eligible, you’ll be pre-approved. You can now make the formal application, which results in a hard credit check. This will show on your credit file.

- You’ll have a credit limit set, based upon your credit score.

- You can choose to flex your payment between 3, 6, and 12 months.

- Interest is charged at 29% APR (variable).

You can use Monzo Flex anytime you use your Monzo card, and even Flex purchases you have made in the previous two weeks.

Like other types of credit, you’ll need to ensure that you can afford the repayments. If you miss a payment, Monzo will provide a grace period of 7 days for you to make the payment. If you cannot do this, Monzo will attempt to take a smaller payment and lengthen the repayment time – resulting in more interest to pay over a longer period. If this happens, it will affect your credit score.

Monzo Accounts

You can open individual and joint accounts in Monzo, providing you are a UK resident and over 16 (though if you live in the United States, you can also apply for a Monzo account). There are four main accounts: Free, Extra, Perks, and Max. (For Extra, Perks, and Max, you need to be aged 18 or over.)

Here is the lowdown on these account options:

| Free | Extra | Perks | Max | |

| Cost Per Month | £0 | £3 | £7 | From £17 (minimum 3 months) |

| AER (Variable) Interest, Paid Monthly | 4.10% | 4.10% | 4.60% | 4.60% |

| Fee-Free Withdrawals | – | Up to £200 | Up to £600 | Up to £600 |

| UK Current Account | ✔ | ✔ | ✔ | ✔ |

| FSCS Protection (up to £85,000 per person) | ✔ | ✔ | ✔ | ✔ |

| Standard Monzo Features | ✔ | ✔ | ✔ | ✔ |

| Connected Banks & Credit Cards | ✔ | ✔ | ✔ | |

| Virtual Cards | ✔ | ✔ | ✔ | |

| Advanced Roundups | ✔ | ✔ | ✔ | |

| Custom Categories | ✔ | ✔ | ✔ | |

| Auto-Spreadsheet | ✔ | ✔ | ✔ | |

| Credit Insights | ✔ | ✔ | ✔ | |

| 3 Fee-Free Cash Deposits | ✔ | ✔ | ||

| Discounted Investment Fees | ✔ | ✔ | ||

| Annual Railcard | ✔ | ✔ | ||

| Weekly Greggs Treat | ✔ | ✔ | ||

| Personal Worldwide Travel Insurance | ✔ | |||

| Personal Worldwide Phone Insurance | ✔ | |||

| Personal UK & Europe RAC Breakdown Cover | ✔ | |||

| Add family to your insurance and cover for an extra £5 a month | ✔ |

In addition to these personal accounts, you can also open the following account types:

Monzo 16/17 Account

This account has been specifically designed for teenagers. It provides many of the features of an adult’s bank account, but with age-related spending stops. This teen account has the following key features:

- Contactless debit card

- Apple Pay and Google Pay

- Spending budgets

- Split Bills

- Fee-free spending abroad (with limits as per personal accounts)

- Spending notifications

There is no overdraft or borrowing facility with the 16/17 account.

Monzo Business Account

Monzo also offers business accounts that include:

- Free UK bank transfers

- Monzo pots – including spending, saving, and tax pots

- Web access as well as mobile access

- Integrated business tools

- Digital receipts and in-app invoicing

- Multi-user access

- Instant notifications

Open a Monzo Business Pro account for £5 per month, and you’ll receive 6 months of Xero (the accounting software) free.

How Do You Open a Monzo Account?

It’s easy to apply for a free Monzo account. You’ll need to be 16 or older and a UK resident with a smartphone (18 for upgraded accounts). Here are the steps to follow:

- Download the Monzo app onto your smartphone.

- Enter your email address.

- You’ll receive an email from Monzo with a link to verify your email address.

- Back on the Monzo app, enter you name, date of birth, address, and phone number.

- Next, you’ll receive an SMS with a verification code to enter into the app.

Now, Monzo’s back-office system will run anti-money laundering and credit checks. You will also need to upload photographic ID (like a driver’s license or passport) and video yourself using your phone speaking a message that Monzo asks you to convey.

When all your documents have been accepted and your application approved, you will receive your Monzo Mastercard through the post.

That’s it! You can now start to set up your budgeting categories, savings and bills pots, and more.

Monzo Fees & Charges

Unless you are opening a paid-for account, there are no charges to open or manage a Monzo account. However, this doesn’t mean you won’t incur charges.

For example, while all ATM cash withdrawals are free in the UK (though some specific exclusions may apply), if you withdraw more than £200 in a single month while abroad, you’ll be charged 3% on the amount over £200.

If you are a Monzo Free account holder, you’ll be charged to make cash deposits – and those charges can rack up if you are only depositing small amounts in PayPoints. £1 to make a deposit may seem like a paltry amount, but it’s 10% of £10, 2% of £5, and 1% of £100. Plus, you can only deposit £1,000 in any six-month period. Paid account holders have much more flexibility to make free-of-charge cash deposits.

Overdraft and loan charges are pretty hefty, so you should take care if you wish to borrow money: always compare Monzo’s offers with other options (and avoid borrowing if it is possible to do so).

If you lose your Monzo card, you will be charged £5 for a replacement.

To keep fees to a minimum, there are some simple ‘rules’ to follow:

- Pay in more than £500 each month – or have your State Pension or benefits such as Universal credit paid into Monzo.

- Have one or more active direct debits from your Monzo account.

- Hold a joint account with anyone who does any of the above.

- Be a Monzo Plus or Monzo Premium account holder.

Is Your Money Safe with Monzo?

It’s natural to worry about being scammed when you are using online apps, especially financial apps. However, Monzo’s account opening processes – including two-step verification and video verification ─ are reassuringly rigorous. A scammer would need your photo ID and a made-to-measure facemask that makes them identical to you to fool Monzo’s systems.

Of greater concern is likely to be the safety of the money in your Monzo accounts. The good news is that, because Monzo is a UK bank and regulated by the FCA, it is obliged to do all it can to protect your money and treat all its customers fairly.

Also, your money is protected against unexpected events – like bankruptcy of Monzo – up to £85,000 or £170,000 for a joint account.

What Customers Think About Monzo

Monzo has a 4/5-star rating on Trustpilot, with 77% of reviewers giving a 5-star rating. Among these, a few headlines read as follows: ‘Haven’t looked back’, ‘Outstanding’, ‘Amazing bank’, ‘I love banking with Monzo’, ‘Monzo, modern bank’.

As for my son and daughter-in-law, here’s what they have to say about Monzo:

“It’s better than any bank account we’ve had before in the UK. It’s easy to open, and then the features like budgeting and saving make money management easier, too. We can see how we’ve been spending our money, which is good for identifying spending pitfalls, and the Roundup feature really helps us save without knowing it!

“Being able to run our bank account on our terms from our home – or anywhere we happen to be ─ is much better than wasting so much time queuing in a bank when all its staff have disappeared for lunch.”

Alternatives to Monzo

What if you don’t like the look of Monzo? It just may not be quite what you’re looking for. Fortunately, there are alternatives. Here are two we would also consider:

Revolut

Revolut has a bunch of great features, and could be ideal if you are travelling abroad ─ it’s cheap and offers top exchange rates. It offers a lot of budgeting, spending, and saving and investment options, too.

However, Revolut doesn’t hold a UK banking license, so don’t expect it to replace your primary UK bank account. Its free account is also more limited than Monzo’s.

Starling Bank

Monzo’s app is a little more friendly than Starling’s. For example, it will alert you when you are near to being overdrawn or you are about to break one of your budget limits. However, you’ll be paid interest on your account balances, and overdraft rates are a little cheaper overall.

Like Monzo and Revolut, you’ll benefit from no-fee spending abroad. You’ll also have access to a range of other financial services through its app.

The Bottom Line

Monzo may have started its life as a simple pre-paid card, but it has evolved into one of the most popular challenger banks in the UK.

Its appeal lies in the wide range of features it offers to make managing your finances easier. Whether you need help with budgeting and keeping on top of spending, saving more easily and effectively, or you want a card that you can use abroad with low or no fees, then Monzo could be what you are seeking.

On top of this, features such as Monzo Flex add more convenience to your cashflow management strategies.

However, you’ll need to decide which of the four account options – Free, Extra, Perks, or Max – is best for your needs, and provides the features you need at an appropriate price point.

You should also be mindful of potential fees and charges, especially with overdrafts and loans, as they can be quite substantial. Comparing these offerings with other options is essential to make informed borrowing decisions.

In the final analysis, Monzo’s branchless, app-driven approach provides you with a modern, user-friendly experience.

I’ve been watching my son’s approach to money over the last few years. I firmly believe that Monzo has helped him to mature financially, and will continue to be a key part of his financial health for many years to come as it evolves its offering in line with the needs of its customers.