Do you want a simple, no-fuss home for your pension investments? In this article, I review two of the most popular pension providers to people like you: Moneyfarm and Penfold.

I compare key factors, including costs and investment options, to help you select the best option for your retirement planning.

Quick Verdict

Both Moneyfarm and Penfold offer hassle-free investment options if you are investing for retirement.

Moneyfarm offers a pension solution tailored for individuals who prefer a hands-off investment approach. With a minimum investment of £500 and no ongoing monthly contributions required, it is a viable option if you can make an upfront investment and prefer to have your portfolio managed by professionals.

The fee structure is transparent and reduces as your investment increases, making it cost-effective for growing portfolios. It’s a great choice for beginners.

Penfold is designed with flexibility in mind, making it ideal if you are self-employed or have a variable income. There’s no minimum investment to start, and you can benefit from a free-to-use lost pension search.

You’ll benefit from fast digital set-up of a range of investment plans to suit your ethical and risk preferences. Its fee structure is also transparent, with management fees that decrease for portfolios over £100,000. Penfold’s ease of use and flexible contribution options make it a strong contender if you seek a customisable and adaptable pension plan.

*Capital at risk

At-a-Glance Comparison

| Moneyfarm | Penfold | |

|---|---|---|

| Range Of Investments | 7 ETF portfolios | 4 Plans: Standard, Sustainable, Sustainable Lifetime, Shariah |

| Done-For-You Investments | £500 | No minimum |

| Set-Up Fee | None | None |

| Account Fee | Included in single pricing format | Included in annual management fee |

| Fund Management Charges | 0.35% to 0.75% Depending on portfolio value | 0.75%, or 0.88% for Sharia plan |

| Exit Charges | None | None |

| Charge To Take Benefits From The Pension | None | None |

Moneyfarm for Pensions

While you may see the Moneyfarm pension quoted as being a SIPP (Self-Invested Personal Pension), it is far from this.

You can’t invest in a broad range of investment instruments, and the investments made are determined by a questionnaire – Moneyfarm is a robo-advisor, after all.

Minimum Investment

You’ll need to invest a minimum of £500 to open a pension with Moneyfarm, though there is not a minimum monthly contribution amount. This initial investment can be made by transferring other pensions into the Moneyfarm pension, or as a cash lump sum.

Transferring In

If you wish to transfer in existing pensions, Moneyfarm will do the donkey work for you free of charge. You’ll need to supply a few basic details, including:

- Current provider’s name

- Your pension account number

- The value and valuation date of your pension

You won’t be charged for this service, and Moneyfarm says the whole process should only take three or four weeks. In my experience, pension transfers often take longer than this.

What Can You Invest In?

When you open a pension with Moneyfarm, you’ll need to complete a simple questionnaire designed to assess your investment and risk profile. This is the robo-advice equivalent of meeting with a financial advisor.

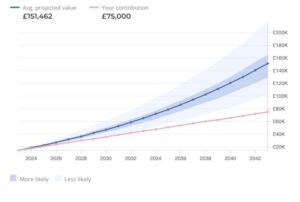

Based upon your questionnaire, you’ll be recommended to invest in one of its seven portfolios of ETFs created by its investment team. Your investment profile is reviewed at regular intervals, and at least once a year (you’ll receive a reminder to do this online).

The portfolios are ‘target-dated’, meaning they de-risk the closer you get to your anticipated retirement age, and in line with your current investment profile. It’s a form of lifestyle, passive fund management. It’s done for you, with no option to select your own investments.

Costs

Here’s one of Moneyfarm’s major selling points – the simplicity and transparency of its fee structure:

There are no fees to set up a Moneyfarm pension. All other fees are included in a single pricing format, based upon the value of your portfolio (Edit: Checked June 2024):

- from £500: 0.75%

- from £10k: 0.70%

- from £20k: 0.65%

- from £50k: 0.60%

- from £100k: 0.45%

- from £250k: 0.40%

- from £500k: 0.35%

The fee you pay is based upon the value of your entire portfolio, meaning as you move to the next level the percentage of what you pay on your portfolio will reduce.

Exit Charges

Should you wish to transfer your Moneyfarm pension to another provider, you won’t be charged to do so.

When it comes to taking benefits from your pension (currently for the age of 55, which is rising to 57 from 2028), there are no charges for putting the plan into drawdown.

*Capital at risk

Investment Platform

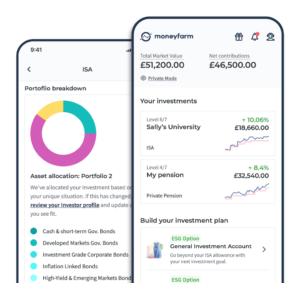

There is no investment platform with the Moneyfarm pension – you don’t need one.

You’ll be able to see the funds you are invested in, their performance, and the portfolio of your fund, but there is no need for more than this.

If you are unhappy with the result of your investment questionnaire, you can retake it.

In effect, you get a mix of active and passive fund management – Moneyfarm’s team manage the portfolio for you, and select the passively-managed ETFs (Exchange-Traded Funds) to hold in the portfolio.

The portfolios are rebalanced three or four times in any 12-month period.

Financial Advice

Moneyfarm’s pension service is delivered with a combination of online robo-advice and its discretionary fund management. The questionnaire creates your investor profile by considering factors such as your financial goals, time horizon, and attitude to risk.

Customer Support

You also get access to a personal investment consultant, who you can meet in person or chat to online, on the phone, or via email. You’ll also find many of your questions are answered in its online help resources.

Should You Use Moneyfarm for Your Pensions?

On the plus side, Moneyfarm makes investing simple. You don’t need to lift a finger, other than complete the investment questionnaire, and fund your account. While only seven portfolios appears very restrictive, they have been designed well to cater for the gamut of investor profiles.

It’s an easy-to-use, free-to-set-up pension that takes you out of the challenging decision-making process when selecting investments. Especially for beginners, I like this simplicity and hassle-free approach: you’ll get a portfolio designed to align with your investment profile while the funds are managed by human beings.

On the other hand, if you want a more active role in determining your own investment portfolio, then you’ll probably be better to consider more traditional low-cost SIPP options, such as that offered by AJ Bell.

*Capital at risk

Penfold for Pensions

Penfold offers an easy-to-understand digital pension product, which you can set up in only a few minutes. There are four investment plans to invest in – Standard, Sustainable, Sustainable Lifetime, or Shariah.

Minimum Investment

There is no minimum investment required to open a pension with Penfold. With no minimum investment and the potential to make one-off contributions, the flexibility this gives makes Penfold a good option if your income is inconsistent.

Transferring In

Penfold offers a free service to transfer existing pensions into your Penfold pension. This includes a ‘Find My Pension’ service to search for and identify lost pensions.

You don’t need to lift a finger, other than fill in a form to get the ball rolling. You’ll also receive updates on progress on your Penfold dashboard (more about this later).

What Can You Invest In?

When you open a Penfold pension account, you’ll need to select which investment plan you wish to use:

1. Standard

Designed to accommodate four different risk profiles. This uses BlackRock iShares to invest in tracker funds.

2. Sustainable Lifetime

A lifestyle-type plan that shifts your investment from growth through ‘preparation’ and finally to ‘protection’, using either standard or sustainable portfolios invested in BlackRock iShares tracker funds.

3. Sustainable

Based on environmental, governance, and social (ESG) criteria. This caters for three risk levels, and invests in BlackRock iShares tracker funds and ETFs.

4. Sharia

Invests in the HSBC Islamic Global Equity Index Fund to track the world’s 100 largest stocks that align with Islamic investment guidelines.

Costs

Like Moneyfarm, Penfold operates a transparent pricing schedule:

- No set-up fees.

- No charge to transfer in.

- Annual management fees of 0.75% for a portfolio value of below £100,000 in the Standard, Lifetime, and Sustainable plans. This reduces to 0.4% above £100,000. For the Sharia plan, the annual management fee is 0.88% for portfolios below £100,000, and 0.53% over £100,000.

There may be other fees payable (such as transaction costs incurred by the fund managers). These are estimated at around 0.10%.

Exit Charges

There are no exit charges, and no charges to make withdrawals when you are able to do so (from age 55 currently, rising to age 57 from 2028).

Investment Platform

There are a few features that help to make pension investing easy.

The pension calculator will help you to see if how much you are investing will put you on track to achieve an income of two-thirds of your current income when you retire. You’ll enjoy playing with the inputs and seeing how they affect the result.

There’s an ‘Explore Your Pension’ feature that lets you see exactly how your pension is invested – and you can even vote at AGMs if you wish!

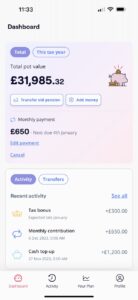

You can also set up direct debits, make lump sum payments, and organise ‘payment holidays’ on the app. It’s clean and easy to use, and keeps you updated on how you are progressing on the road to your retirement.

Something else I like is the ‘Beneficiaries’ section. You can bequeath the fund should you die, and this feature makes it easy to do so.

Financial Advice

No financial advice is available, except for its robo-advice features.

Customer Support

There are two ways of getting in touch if you need help. The first is an online chat function that is available between 7am and 4pm each weekday.

If this is unavailable, you can also send a message with your query and the support team will get back to you when they become available.

Should You Use Penfold for Your Pensions?

Though the Penfold pension was designed with the self-employed in mind, if you want a low-cost, flexible pension plan that is easy to set up and will help you to invest according to your current investment profile, then this could be a good choice for you (though you should also check out PensionBee).

If you have other pensions to transfer in, or if you may have lost pensions, its free pension finding and transfer service could prove invaluable.

*Capital at risk

Why Costs Matter

Even though the difference between, say, a 0.5% annual management charge and a 1% annual management charge seems minimal, a small difference can have a big impact on your final pension fund over time. As your retirement income depends upon this, the costs associated with your pension should always be a factor you consider.

Here’s a simple example (not allowing for inflation) of how costs can impact your investment:

| Value Of Fund At Set-Up, With No Further Contributions | Gross Average Annual Return | Annual Costs | Value After 10 Years | Value After 25 Years |

| £100,000 | 5% | 0.25% | £159,052 | £319,042 |

| £100,000 | 5% | 1% | £148.024 | £266,583 |

| £100,000 | 7% | 0.25% | £192,167 | £511,912 |

| £100,000 | 7% | 1% | £179,085 | £429,188 |

When you see this in print, it really drives home why costs matter, doesn’t it?

5 Tips to Help You Decide

Choosing the right pension provider can be like walking through a maze. You want to get to the centre as quickly as possible, but taking a wrong turn can have disastrous consequences.

To help you avoid dead-ends and turns that take you back to the starting line without achieving your goal, here are my tips for choosing the best pension provider for you:

Assess Your Investment Approach

Reflect on whether you prefer a passive role or an active one in managing your investments.

Check if the Minimum Investment Fits Your Budget

It’s important to determine whether the required initial investment is feasible for you.

Consider the Impact of Fees on Your Pension

Always factor in how various charges might influence your investment’s growth over time.

Scrutinise the Range of Investment Choices

Ensure that the available options resonate with your investment style and financial objectives.

Examine Transfer Procedures & Extra Costs

When thinking about switching from another pension plan, always weigh the potential expenses against the points mentioned above.

The Verdict

Have you narrowed down the choice of pension provider to Moneyfarm or Penfold? Here’s a summary of what they both have to offer:

Moneyfarm has redefined pension investment with its robo-advisory approach. Though you must open with a minimum investment of £500, there are no minimum monthly contributions.

It streamlines the transfer of existing pensions at no cost, and guides your investment through a questionnaire that leads to one of seven portfolios invested in a range of ETFs. These portfolios adapt to your retirement timeline and risk profile. Moneyfarm’s fee structure is transparent and tiered, decreasing as your investment grows.

Penfold offers a digital, user-friendly pension solution that is ideal if you have a varied income. It simplifies setting up and transferring existing pensions, and includes a free service for tracing lost pensions.

There are four investment plans to choose from – Standard, Lifetime, Sustainable, and Shariah – mostly using BlackRock iShares tracker funds to match your investment to your investment profile. Penfold’s transparent fee structure is based on portfolio value, and the app features tools like a pension calculator.

Enabling flexible contribution options, Penfold is particularly suitable if you are self-employed or may wish to pay in varying levels of contributions.

When you are choosing a pension provider, always consider your investment style, your experience, and the costs associated with the pension plan you are considering.

*Capital at risk